CHAPTER 12 : MUTUAL FUND SCHEME SELECTION

SCHEME SELECTION BASED ON INVESTOR NEEDS, PREFERENCES AND RISK-PROFILE

1. Investor Need: The investor may need long term appreciation in the value of his investment, or the investor may need periodic income from the investment, or the investor may be looking for an avenue to park funds and need an investment with high liquidity. Therefore, the first step is to set one’s financial goals.

2. Risk Profile of the investor: The investor’s risk appetite is a function of three things the need to take risks, the ability to take risks, and the willingness to take risks.

3. Asset Allocation: The investor’s asset allocation is a decision regarding how much money should be allocated to which scheme category (asset class). This decision can be taken only after assessing the investor’s risk profile and analysing the investor’s goals and situation.

4. Age of the investor: One of the common factors that many people use to evaluate the investor’s risk profile is the investor’s age Different investors have different financial goals at different age levels. In fact, investors in the same age group may also have different goals.

5. Investment Horizon: Longer the horizon to the goal, the ability to take risks is higher, whereas one may avoid risks when the goal is in the near future.

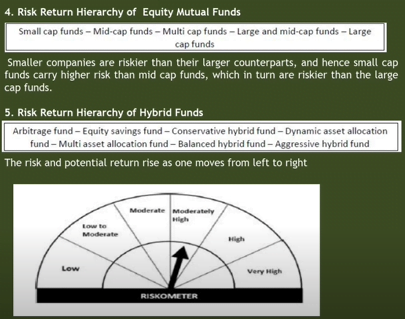

6. Core and Satellite Portfolio: It is good to consider the role that the scheme will play in the investor’s portfolio. Ideally the portfolio should be divided into core and satellite portfolios. The core portfolio will be invested according to the long-term needs and goals of the investor. The satellite portfolio will be invested to take advantage of expected short-term market movements. For example, a diversified equity fund, large cap, mid-cap funds, among others may form part of the core portfolio since they generate long-term returns in broad alignment with the markets.

SELECTING OPTIONS IN MUTUAL FUND

The underlying returns in a scheme, arising out of its portfolio and cost economics, is what is available for investors in its various options.

Income distribution cum capital withdrawal (Dividend) payout option has the benefit of money flow to the investor and seems attractive for investors wanting a regular income.

Growth option has the benefit of letting the money grow in the fund on gross basis (i.e., without annual taxation).

Re-purchase transactions are treated as a sale of units by the investor. Therefore, there can be an element of capital gain (or capital loss), if the re-purchase price is higher (or lower) than the cost of acquiring those units.

Dividend income is subject to tax as per the applicable tax slab of the respective investor. The tax on dividend reduces the returns for the investor. Thus, Income distribution and capital withdrawal (dividend) option is not preferable, except in the case of tax-exempt investors.

The need for regular income is better met through a SWP for the requisite amount. Sale of units under an SWP may have STT implication (equity schemes) and capital gains tax implications (equity and debt schemes.

SELECTION OF MUTUAL FUND SCHEME OFFERED BY DIFFERENT AMCS OR WITHIN THE SCHEME CATEGORY

Fund Portfolio: The fund’s portfolio has to be evaluated to determine the risk and return in the scheme.

Fund Age: A fund with a long history has a track record that can be studied. Fund age is especially important for categories of schemes, where there are more investment options, and divergence in performance of schemes within the same category tends to be more.

Fund Size: The size of funds needs to be seen in the context of the proposed investment universe. A large fund size will allow better diversification and economies of scale. A small sized fund on the other hand is more flexible and better able to take advantage of market

opportunities.

Portfolio Turnover: Frequent churning of the portfolio would not only add to the broking costs, but also be indicative of unsteady investment management. Portfolio Turnover Ratio is calculated as Value of Purchase and Sale of Securities during a period divided by the average size of net assets of the scheme during the period.

Scheme Running Expenses: Any cost is a drag on investor’s returns. Investors need to be OM WISD particularly careful about the cost structure of debt schemes, because in the normal course, debt returns can be much lower than equity schemes.

Growth or Value funds:

Funds that follow the growth strategy seek to identify companies that are expected to grow at rates higher than the average economic growth rate. Stocks of such companies tend to do well in a bull phase in the markets. But in a market downturn the price of such stocks tends to fall much more too, making them riskier.

Value strategy seeks to identify stocks that are available at a price that is seen as cheap relative to the value that could be unlocked in the future.

Gold Funds

Investors need to differentiate between Gold ETF and Gold Sector Funds. The latter are schemes that invest in shares of gold mining and other gold processing companies. The performance of these gold sector funds is linked to the profitability of these gold companies unlike Gold ETFs whose performance would track the price of gold.

Hybrid Schemes:

Investing in a hybrid scheme makes things simpler for the investor, because fewer scheme selection decisions need to be taken. However, the investor would need to go by the debt- equity mix in the Investment portfolio of the schemes.

The equity component in a hybrid fund provides the appreciation in value, while the regular returns from the debt component provide the stability to the returns.

International Equity Funds:

When an Indian Investor invests in equities abroad, he is essentially taking two exposures:

- An exposure on the international equity market.

An exposure to the exchange rate of the rupee.

Taking this kind of exposure is possible and convenient through the international equity funds, which invest in stocks of companies listed in stock exchanges located outside of India.

Fixed Maturity Plans

These are close-ended debt funds. Fixed Maturity Plan is ideal when the investor’s investment horizon is in sync with the maturity of the scheme, and the investor is looking for a more predictable return than any conventional debt scheme, and a return that is generally superior to what is available in a fixed deposit.

Short Duration Fund

Short Duration Funds invest in securities with maturities between 1 year and 3 years. As such they earn returns in line with the market yields.

Liquid Funds

An investor seeking the lowest risk ought to go for a liquid scheme. However, the returns in such Instruments are low.

DO’S AND DON’TS WHILE SELECTING MUTUAL FUND SCHEMES

While selecting the mutual fund schemes, there are few things that a mutual fund distributor must keep in mind. Some of them are listed below:

- Ensuring suitability

- Sticking to investor’s asset allocation

- Chasing past performance

- Understanding the investment objective and investment strategy of the scheme.

- Developing a consistent methodology for scheme selection.

- Keeping an eye on the taxes and loads.

CHAPTER 1: Investment Landscape

CHAPTER 2 : Concept And Role Of A Mutual Fund

Chapter 3: Legal Structure Of Mutual Funds In India

Chapter 4: Legal And Regulatory Framework

Chapter 5: Scheme Related Information

Chapter 6: Fund Distribution & Channel Management Practices

Chapter 7: Net Asset Value, Total Expense Ratio & Pricing Of Units

Chapter 10 : Risk, Return And Performance Of Funds

3 thoughts on “Chapter 12 : Mutual Fund Scheme Selection”